Contact Sales (402) 933-4864

Written by: Zac Robinson

The old saying goes, “If it ain’t broke, don’t fix it.”

This saying may be true for more than just a few things in life—your refrigerator, your car, your coffee maker, etc.—but your company’s accounts receivables operations (and the technology that supports it) isn’t one of them.

The new version of this old saying goes more like this:

“’If it ain’t broke, don’t fix it’ is the slogan of the complacent, the arrogant or the scared. It’s an excuse for inaction, a call to non-arms.” – Colin Powell

Many an A/R department has operated behind the curtain of “We’ve just always done it this way,” acknowledging that while legacy technology and processes that are well past their prime are still being used within critical A/R operations, they don’t believe they have uncovered a pressing need to upgrade their systems and processes.

But that’s just the problem, many companies’ A/R operations are broken, whether or not they choose to recognize it. Tedious, manual, error-prone tasks lurk behind every touch-point, ready to jump on the pile of work required to accept, process and ultimately apply payments across numerous, disparate, out-of-date systems that slow down and complicate A/R operations.

While slow, highly-laborious processes and aging technology remains in place within companies’ A/R operations, the entire payment landscape is changing. Customers payment preferences are quickly accelerating towards electronic payments. But checks are still alive and well, and not going away anywhere near as fast as some parties may like to claim.

While slow, highly-laborious processes and aging technology remains in place within companies’ A/R operations, the entire payment landscape is changing. Customers payment preferences are quickly accelerating towards electronic payments. But checks are still alive and well, and not going away anywhere near as fast as some parties may like to claim.

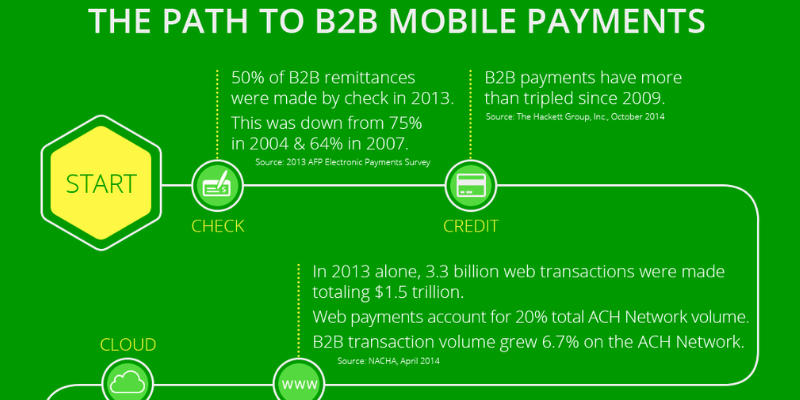

Recent research from CRF and NACHA illustrates the breakout of shifting B2B payment landscape as follows:

CRF and NACHA go on to estimate that ACH payment volume will increase to account for 45% of B2B payments by 2020, while check and card payments will decrease to 34% and 12.5% respectively, and cash and wire will increase slightly to 8.5%.2

So, the question that you are likely left asking is, “How can we adapt to such rapid change, and who is best suited to help us manage this evolution?”

As customers payment preferences have changed over the years, businesses have been forced to adapt their systems and processes to accommodate new payment methods and channels. All too often, this adaptation has involved adding new systems that lacked integration and depended on high-touch, highly manual processes that hindered operational efficiency.

While banks have historically been the first-place corporate customers turned for payment processing services such as remote deposit capture (RDC), ACH acceptance and merchant services, FinTech providers have made significant strides in adoption within corporate customers over the past 5-10 years.

What is driving the shift?

Recognizing the need for greater flexibility and oversight within their A/R operations, corporate treasury professionals have identified the value integrated receivables solutions can deliver their organizations. According to a recent survey by the Aite Group, 73% of corporate treasury professionals say a bank’s ability to provide an integrated receivables offering is ‘important’ or extremely important’ when selecting a new banking partner.4

Naturally anxious to meet the expectations of their corporate banking customers, another recent Aite Group survey shows that banks have heard the call, reporting that 70% of banks rank integrated receivables technology as a ‘high’ priority.3

Here’s where we come upon the disconnect between banks’ reported priorities and the action required to actually deliver corporate customers with the technology they want and need. In order to do this, banks have to fundamentally shift how they approach selling value-added solutions—not necessarily something that has been a notable strength for banks’ sales organizations through the years.

Simply seeking out and offering low-cost, point solutions will no longer cut it. Business customers will always want a competitive price, but with low prices come low value solutions. Low prices and low value solutions are what got them ‘here’, they are not what will get them ‘there’.

Aite Group reported that 31% of banks were only in the “planning” stage of rolling out an integrated receivables solution during 2017.3 What’s more, Aite Group went on to reveal that 50% of banks were still 3+ years away from rolling out the technology.3

These are concerning stats when you step back to consider the fact that the vast majority of banks are far more likely to partner with a FinTech provider to bring an integrated receivables solution to market than build the technology themselves. Is it ‘really’ a priority if customers are going to have to wait 3+ years for the technology and solutions that are readily available today?

Despite the buzz integrated receivables solutions have started to generate over the past several years, they’ve been here for a while now. They are being used by leading companies across numerous industries. It does not take years to roll-out this technology. In fact, a growing number of innovative community and regional banks understand the opportunity before them in partnering with FinTech providers to gain a first-mover (at least in comparison to other banks) advantage in delivering truly integrated receivables solutions to their corporate banking customers.

Simply having technology in place is not enough to maximize operational efficiencies. It has to be the right technology. Preferably a system that can provide the flexibility to evolve with your ever-changing accounts receivables needs. If you’re a bank, any solution you provide your corporate banking customers should make their lives easier, not harder. Your customers should benefit from solutions that can be configured to their business and technological requirements. They shouldn’t be forced to change their operations and processes to ‘fit’ into the parameters of a rigid, legacy system.

Most companies (including banks) already have the basic capabilities in place to allow customers to pay via multiple payment methods. The problem lies in the inconvenience of having to manage multiple platforms to effectively manage and oversee each of those payment methods—not to mention still having to endure the pain of manually entering remittance and payment details into your back-office system(s). And what happens when your customers start requesting new payment channels such as online or mobile?

Any time customer requests start to pile up for new features or functionality, it’s easy to let our near-term needs blind you from your long-term vision and how best to get there.

While it may seem that your customers’ payment preferences are shifting towards electronic payments at an accelerated pace, industry statistics show that the evolution isn’t happening nearly as quickly as it may seem. After all, if you have more than one customer, it is very likely that you will need to be able to provide more than one payment method and channel for the remittance of payments. The key is to be able to provide the appropriate mix of customer-facing payment methods, channels and interfaces while also maximizing internal operational efficiencies associated with cash application into your back-office system(s).

According to AFP’s 2016 Electronic Payments Survey, 94% of companies continue to use checks to pay their major business suppliers.5 And while 80% of businesses report ACH remittance as their preferred payment method from their customers,5 21% of companies say they do not have the proper system in place to accept ACH payments.2 Another 34% of companies report that while they can accept ACH payments, they receive them without the proper remittance data.2

All of this focus on accepting ACH payments is taking place while 55% of organizations now report the ability to accept credit card payments from customers.5

If nothing else, two things are for sure: 1) Even though electronic payments are the future, they still present plenty of operational challenges today as 69% of companies report a lack of integration between electronic payments and accounting systems to be a key barrier to further adopting electronic payments within their A/R operations;5 and 2) The ability to deploy flexible, highly-configurable and seamlessly integrated receivables solutions has never been more important.

Unfortunately, it may not always be as easy as it should be to put an exact number on the dollars and time inefficient processes and disparate systems are costing your business because it can be different for each individual business. But rest assured, you’ll know it when you see it.

Just as the mounting costs surrounding inefficient, siloed A/R systems and processes can be unique, so can the benefits delivered from the truly integrated solutions that ultimately help you remove the legacy systems that have plagued your operations for far too long.

Whether your goal is to decrease DSO by days, significantly reduce the time it takes to review payment and remittance details, consolidate banking relationships (if you’re a bank that can deliver truly integrated receivables solutions, you should like the sound of this goal), add new payment methods and channels, or achieve straight-through processing, today’s truly integrated receivables processing solutions can help you achieve it.

That’s the beauty of these solutions, they’re modular, so they aren’t limited by any predefined use cases or rigid, standard integrations or data sets. They're designed to be configured to your business needs and requirements, not the other way around.

Need to change back-office systems? No problem.

Adding or consolidating banking or merchant processor relationships? Feel free.

Ready for new check scanning equipment? Have your pick.

Timing is everything in life and in business. Maybe you’re ready to make the move to a truly integrated receivables platform today, or maybe you’re not. Maybe you’re one of the fast-growing number of organizations already benefiting from these transformative solutions. Maybe you’re still hiding behind the veils of “we’ve just always done it this way” or “our processes aren’t broken, why should we fix them?”.

Whatever the case, there is no time like the present to take a step back, remove the emerald colored glasses provided by A/R solutions of the past and take a fresh look at the truly integrated receivables solutions of today and the future.

We think you’ll like what you see.

Sources:

1 | Deloitte | B2B Payments for the Middle Market, 2016

2 | NACHA | 2017 CRF/NACHA Payment Benchmarks

3 | Aite Group | Banks Journey Into Integrated Receivables: A Three-Pronged Approach, 2018

4 | Aite Group | The Corporate Need for Integrated Receivables, 2018

5 | AFP | Electronic Payments Survey, Report of Survey Results, 2016

Originally published on PYMNTS.com on 10/20/2015. For a corporate treasurer to be able to view all...

Read More

Whether you’re one of the world’s largest corporations, a small Internet store or somewhere in...

Read More

To stay ahead of competition, insurance agencies can leverage the latest payments technology to...

Read More

Copyright 2023