Contact Sales (402) 933-4864

.png)

Written by: Colby Ring

Originally published on 6/25/2014.

Updated on 2/16/2022.

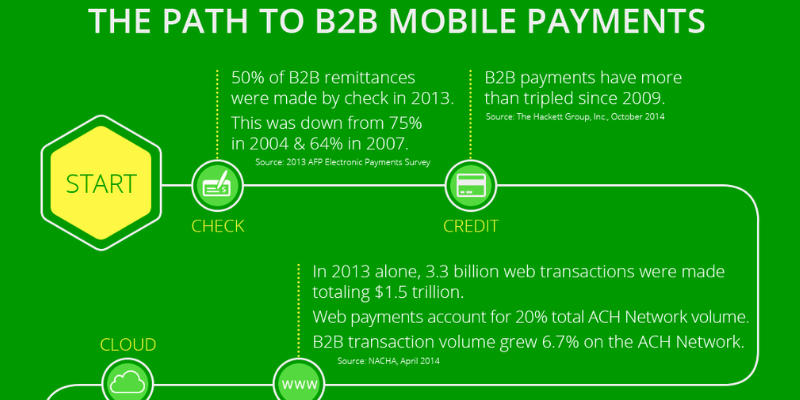

The Automated Clearing House (ACH) is a network that banks use to electronically process payments. ACH payment processing involves tens of billions of transactions. These transactions totaled a monetary value of $36.9 trillion in 2012. The National Automated Clearing House Association (NACHA) and the Federal Reserve both oversee this important money exchange system that handles large volumes of debit and credit transactions in batches.

ACH payment processing is conducted by both the Federal Reserve Banks and the Electronic Payments Network (EPN). The Federal Reserve handles about 60 percent of commercial interbank ACH transactions, and the EPN handles the remaining 40 percent.

The Federal Reserve Banks and the EPN work together when transactions involve payment processing that is not for their customers. Customers generally have no knowledge of which entity handles their funds; they just see that the money has cleared when they check their accounts.

ACH payment processing is generally preferred by businesses over other payment methods that do not involve cash. These payments are received and processed quickly, and the funds are deposited directly to the merchant’s account.

ACH payment mistakes are typically limited and minor. The most common mistakes occur when a customer writes the wrong amount for a check or a check is sent in late. If a bad payment is received, businesses can automate attempts to collect.

One disadvantage with ACH is that businesses have to pay for set-up costs and a fee per transaction. Generally, it is worth the cost as it offsets the expense of collection and bookkeeping. Users should also keep in mind that deposited money is not always available for use immediately. However, processing is much faster than with checks. Another disadvantage is that bounced/returned checks usually show up in 24-48 hours, where as a consumer has up to 90 days to dispute an ACH transaction.

Writing checks is still a common practice, however, it is slowly declining due to the usage of electronic payments in the marketplace. ACH payment processing can be seen as an easier alternative to some businesses and consumers when it comes to making and accepting payments. Checks and stamps are no longer needed and mail delivery issues are virtually eliminated, reducing late fees. ACH payment processing is also less hassle, too, because customers can pay by phone or online. Additionally, customers can also create a hands-off recurring billing schedule with automatic debit payments.

Customers do have to share information about their bank account with a business. Also, customers must keep enough funds in their account or ACH payment processing could overdraw the account, which can cause service fees.

For many small businesses, ACH payment processing offers advantages that make this payment option very appealing. It provides an easy, convenient customer payment method that provides operational efficiency compared to accepting checks or credit card payments.

Small business operators can also use ACH payment processing to handle recurring payments including mortgage, utility bills, and loan payments. ACH is also conducive to handling e-commerce payments and local, state, and federal tax payments.

Let’s face it, the traditional processes surrounding the processing and management of...

Read More

Whether you’re one of the world’s largest corporations, a small Internet store or somewhere in...

Read More

Today’s growing portfolio of payment channels continues to add new levels of complexity to payment...

Read More

Copyright 2023